Knife River (KNF)·Q4 2025 Earnings Summary

Knife River Surges 15% on Record Q4, Smashes EPS Estimates by 37%

February 17, 2026 · by Fintool AI Agent

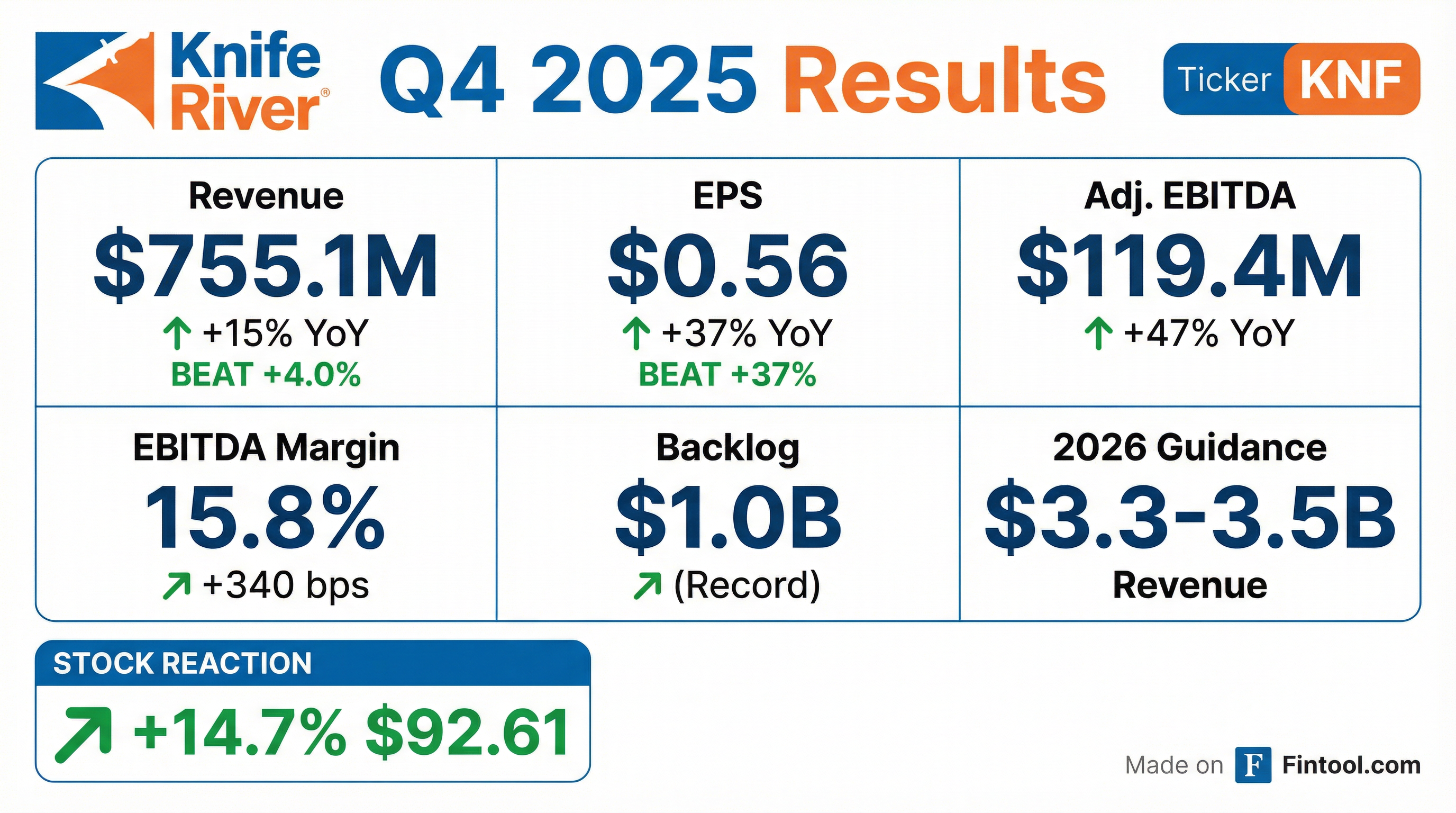

Knife River (NYSE: KNF) delivered a record fourth quarter, with EPS of $0.56 crushing the Street's $0.41 estimate by 37% . Revenue of $755.1 million topped consensus by 4%, driven by an extended construction season and strong contributions from five acquisitions completed throughout 2025 . The stock jumped 14.7% to $92.61 on the news.

CEO Brian Gray called it "a year of meaningful progress" as the company enters 2026 with record $1 billion backlog, favorable public funding tailwinds, and a proven Competitive EDGE playbook driving operational improvements .

Did Knife River Beat Earnings?

Yes — and convincingly. Both EPS and revenue exceeded expectations, while EBITDA nearly doubled estimates on a beat basis.

The Q4 beat extends Knife River's recent track record — the company has now topped revenue estimates in three of the last four quarters .

Key drivers of the beat:

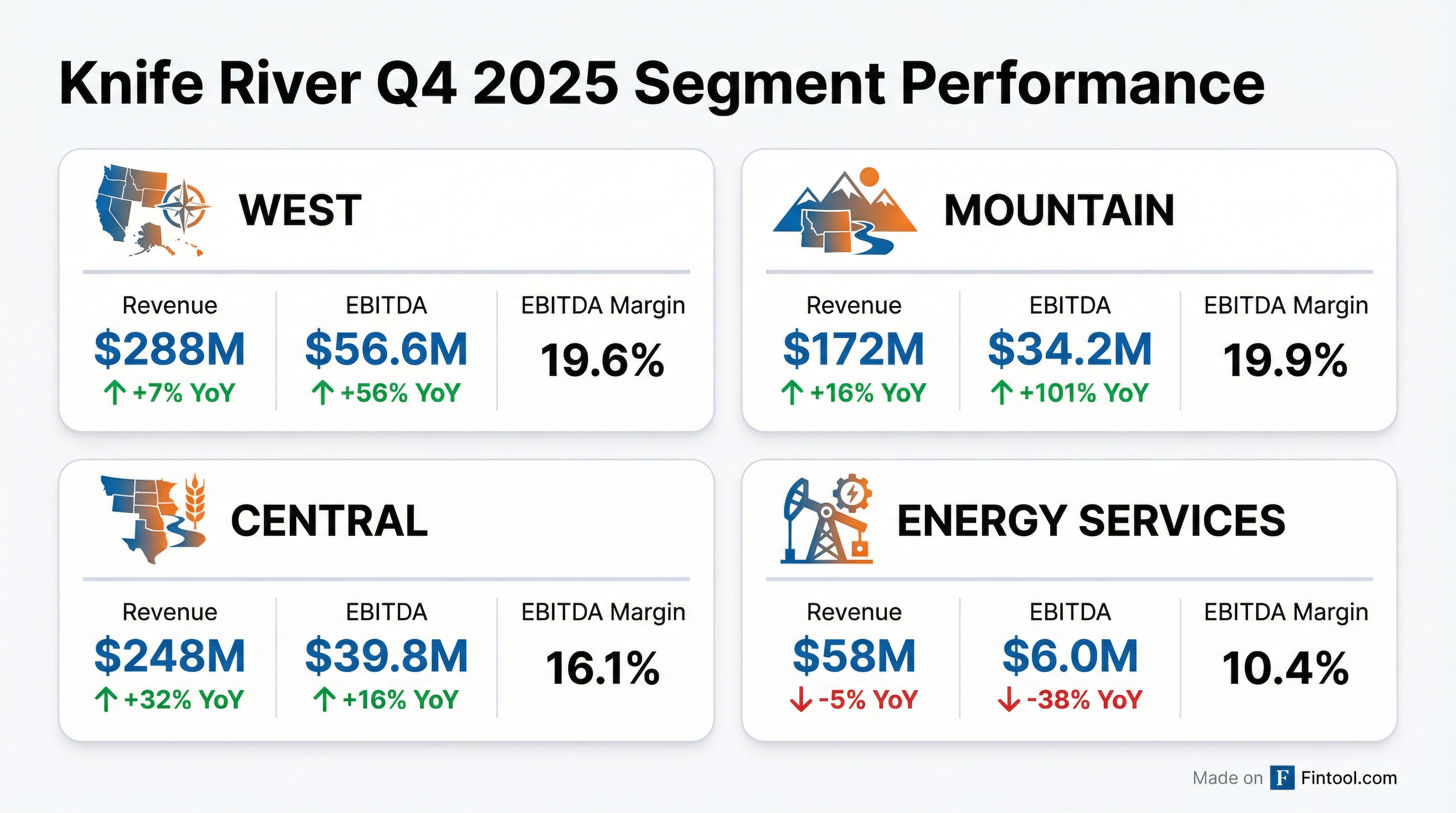

- Favorable weather extended the construction season, particularly in the Mountain region where contracting services revenue jumped nearly 20%

- Acquisition contributions from five aggregates-based deals in 2025, led by Strata and TexCrete which closed in mid-December

- Pricing power with aggregate ASP up 8% YoY (mid-single digits at legacy operations) through dynamic pricing discipline

- Volume growth across aggregates (+17% YoY) and ready-mix (+20% YoY) supported by improved market conditions in the West

- Cost controls — aggregates cost per ton declined in the second half of 2025 vs. prior year period

How Did the Stock React?

KNF shares surged 14.7% to $92.61 following the earnings release, marking the stock's best single-day gain since its spinoff from MDU Resources in 2023. The move pushed shares to their highest level since February 2025.

The magnitude of the beat — particularly the 37% EPS surprise — combined with above-consensus 2026 guidance drove significant upward revision expectations.

What Did Management Guide?

2026 guidance came in above Street expectations, with revenue guidance of $3.3B-$3.5B exceeding the $3.29B consensus .

Key guidance assumptions:

- Aggregates volumes and pricing to increase mid-single digits

- Ready-mix volumes to increase mid-teens (Texcrete expected to more than double Texas Triangle volumes)

- Asphalt volumes to increase mid-single digits

- Energy Services results broadly in line with FY 2025

- D&A to increase mid-single digits

Management noted the guidance excludes potential acquisitions, suggesting upside if M&A activity continues at the pace seen in 2025 .

Q1 2026 seasonality note: Management expects approximately 8% seasonal EBITDA loss in Q1 due to Strata's seasonality (North Dakota winter), though some TexCrete benefit may soften this .

What Changed From Last Quarter?

The narrative shifted from "weather headwinds" to "record results and momentum."

Key shifts:

- Backlog hit a record $1 billion, up from $746M a year ago — providing visibility into 2026

- West and Mountain segments rebounded with EBITDA up 56% and 101% YoY respectively, after Q3 underperformance

- Texcrete acquisition closed in Q4, positioning KNF to double ready-mix volumes in the Texas Triangle

- Net leverage improved to 2.2x from higher debt levels post-acquisitions, still below 2.5x target

How Did Segments Perform?

Standout: Mountain segment EBITDA doubled on late-season contracting work (construction revenue up nearly 20% in Q4), improved cost controls, and favorable weather allowing work into December . Ready-mix margins improved 400 bps as pricing outpaced costs .

Central grew fastest at 32% revenue growth, driven by Strata integration, TexCrete addition, and record DOT budgets in North Dakota and Texas. Central expects its busiest contracting services year ever with the $112M Highway 6 (Texas) and $62M Highway 85 (North Dakota) projects .

Energy Services lagged due to lower oil prices, though expected to remain margin accretive in 2026 with Albina Asphalt operational improvements and higher-margin, value-added product focus .

What Did Management Say?

"Knife River delivered strong second-half results in 2025, including a record fourth quarter that saw a 15% increase in revenue, 47% improvement in adjusted EBITDA and 340 basis-point expansion in adjusted EBITDA margin, year-over-year."

— Brian Gray, President and CEO

"We enter 2026 with momentum and confidence in our strategy to deliver long-term, profitable growth. We have record year-end backlog of $1 billion, which includes the opportunity to pull through our higher-margin materials."

— Brian Gray

Key strategic priorities for 2026:

- Continue materials pricing optimization and plant efficiency improvements

- Maintain M&A activity with pipeline similar to 2025

- Invest in organic growth focused on highest-return areas

Q&A Highlights

Data Center Opportunity — "Never Seen This Level of Pending Work"

Asked about data center exposure, CEO Brian Gray revealed significant upside potential not reflected in guidance:

"Virtually zero amount of dollars in our backlog are related to data centers... We are currently working on 21 data centers, and again, most of that would be through the supply of aggregates or concrete... The amount of work that we have out there pending, bids that are out there that we have provided in the last two months, it's significantly more than what we currently have supply contracts for."

— Brian Gray

Data center opportunities span multiple states including Wyoming, North Dakota, and Oregon — all in KNF's core footprint with existing aggregate and ready-mix plants .

3-Year Margin Expansion Progress

When asked about the path to the 20% EBITDA margin target, Gray highlighted impressive gross profit margin gains over the past 3 years:

Oregon and West Backlog Shift

Analyst Brent Thielman asked about the West segment's lower backlog contribution. Gray acknowledged the geographic shift but expressed confidence:

"We definitely have seen a shift, a geographic shift of that work, more in Mountain with a record backlog and Central with a record backlog. But we have very solid funding in California, Hawaii, and Alaska... The DOT budget in Oregon is about flat, slightly up a little bit, and the asphalt paving tonnage is also slightly up for this year."

— Brian Gray

Oregon's legislature is currently discussing infrastructure funding in its short session, with a larger, longer-term bill expected to pass in 2027 .

Dynamic Pricing Implementation

On pricing levers, CFO Nathan Ring noted that all legacy sites have now fully implemented dynamic pricing, allowing continuous price optimization rather than annual price letters . As acquisitions are completed, dynamic pricing tools are rolled out to new sites.

M&A Track Record and Pipeline

Gray emphasized Knife River's proven M&A playbook:

"We've done almost 100 deals now since the early 1990s... It's very focused on getting the right deals in the pipeline, being very disciplined at the deals we put in the pipeline and going out and courting those relationships."

— Brian Gray

The pipeline remains "robust and full" with deals similar in type, size, and location to the five completed in 2025 — aggregates-based, vertically integrated bolt-ons in mid-sized, higher-growth markets .

Full Year 2025 Recap

"Knife River has enjoyed considerable growth over the last three years, with revenue improving by 24%, adjusted EBITDA by 58%, and adjusted EBITDA margin by 340 basis points."

— Brian Gray, closing remarks

Why net income declined: Higher interest expense (+$26M YoY) from debt taken on for acquisitions offset operating improvements . On an EBITDA basis, the business delivered solid growth.

Capital allocation highlights:

- $789M total growth investment across acquisitions, reserve expansions, and organic projects

- $170M on maintenance capex (6% of revenue, within 5-7% target range)

- $131M planned for organic growth in 2026 including reserve additions

Balance sheet strength for continued M&A:

- $75M unrestricted cash

- $475M available on revolver

- Net leverage at 2.2x (below 2.5x target; willing to go to ~3x for the right deal)

- Cash flow from operations expected at ~2/3 of EBITDA in 2026

Key Risks and Concerns

-

Backlog margins expected to compress — management noted margins on $1B backlog are expected to be lower than year-ago backlog

-

Weather dependency — Q4 benefited from unusually favorable weather; adverse conditions could pressure 2026 results

-

Energy Services weakness — segment saw EBITDA decline 38% YoY on lower oil prices; if oil weakness persists, could be a drag

-

Integration risk — five acquisitions in 2025 creates execution risk around synergy capture

-

Leverage at 2.2x — while below 2.5x target, limits flexibility for opportunistic M&A

Forward Catalysts

- Q1 2026 earnings — seasonal loss quarter (~8% of full-year EBITDA loss expected); Street expects EPS of -$1.35 on $373M revenue

- Texcrete integration progress — more than doubles Texas Triangle ready-mix volumes

- M&A pipeline — management indicated deal flow similar to 2025; already completed one bolt-on in Montana and expects more before construction season

- IIJA funding acceleration — approximately 46% of IIJA funds in KNF's 14-state footprint remains to be disbursed

- Data center demand — currently working on 21 data centers; significant pending bids represent upside to guidance

Key Financial Data

Quarterly Trend (Last 8 Quarters)

*Values retrieved from S&P Global

Product Line Performance (Q4 2025)

This analysis was generated by Fintool AI Agent based on company filings, earnings materials, and market data as of February 17, 2026.